table of contents

Many healthcare professionals are not registered for GST/HST because they are not required to do so. That’s because the services they provide fall under the category of exempt services under the Excise Tax Act. But, in the last couple of years, the interpretation of what is considered to be an exempt service (versus non-exempt medical services) has been more precisely defined. Now healthcare professionals need to consider whether or not their activities are either exempt or non-exempt services. More often than not they are both!

Do You Provide Non-Exempt Services?

For those healthcare professionals not registered, they may be subject to GST/HST yet be unaware of their obligation under the Excise Tax Act. This is an issue that should be raised by their accountant. Unfortunately, it is often overlooked but not without consequence.

For those healthcare professionals already registered, they (and their accountants) should be aware of the various supplies and services subject to GST/HST.

Non-Exempt Services More Than $30,000 Per Year

When non-exempt services are provided, in excess of the annual threshold for registration ($30,000) a healthcare professional is required to register for GST/HST. Once registered for GST/HST, a healthcare professional has an ongoing obligation to file GST/HST returns whether or not non-exempt services exceed $30,000 per year or not.

Know What Is Exempt And What Is Not

Healthcare professionals, or their accountants, need to distinguish those supplies and services performed for the purpose of the protection, maintenance, or restoration of the health of a person from those which are not. The former are exempt for purposes of GST/HST. The latter are not.

When the value of non-exempt services performed reach $30,000 per year a healthcare professional must register for GST/HST. So, for example, where the total value of medical reports written for insurance companies and block fees collected exceed $30,000 per year, then registration for GST/HST is required.

Other examples of non-exempt services include back-to-work notes, Driver’s License Reports, completion of Disability Tax Credit form, cosmetic surgery and teeth whitening. All examinations and services covered by a provincial health insurance plan remain exempt.

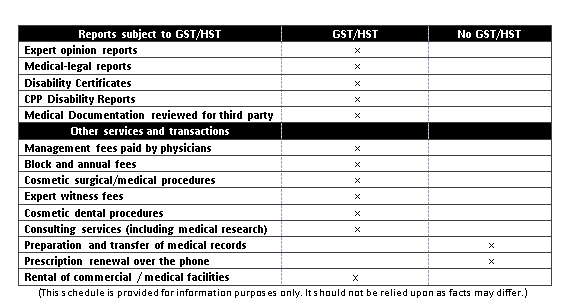

Below is an abbreviated summary of certain healthcare related services and their GST/HST status:

Manage Your Exposure

If you are a healthcare professional providing a variety of healthcare services, your GST/HST obligations should be considered each year by your tax advisor. Your professional activities can change giving rise to GST/HST reporting obligations that can easily go overlooked. Your level of non-exempt activities can exceed $30,000 inadvertently resulting in unintended resulting in unintended GST/HST consequences. If your tax advisor is not addressing this with you, ask them whether or not GST/HST is applicable in your circumstances. They may not have considered this. If you’re concerned that this is being overlooked get a second opinion; be proactive.

For assistance with GST/HST, other tax, and business advisory matters, or for a second opinion, contact Jonathan at 1-800-845-0540 or by email to [email protected].