table of contents

If you’ve received an instalment reminder notification from Canada Revenue Agency (“CRA”) by mail or through your CRA portal—pay attention to it. The notifications you receive are legally binding, and the fact that you’ve received a notification obliges you to take action in some form or other.

That action includes assessing whether you owe the amount set out in the instalment reminder or a lesser amount. In any case, please don’t ignore this reminder.

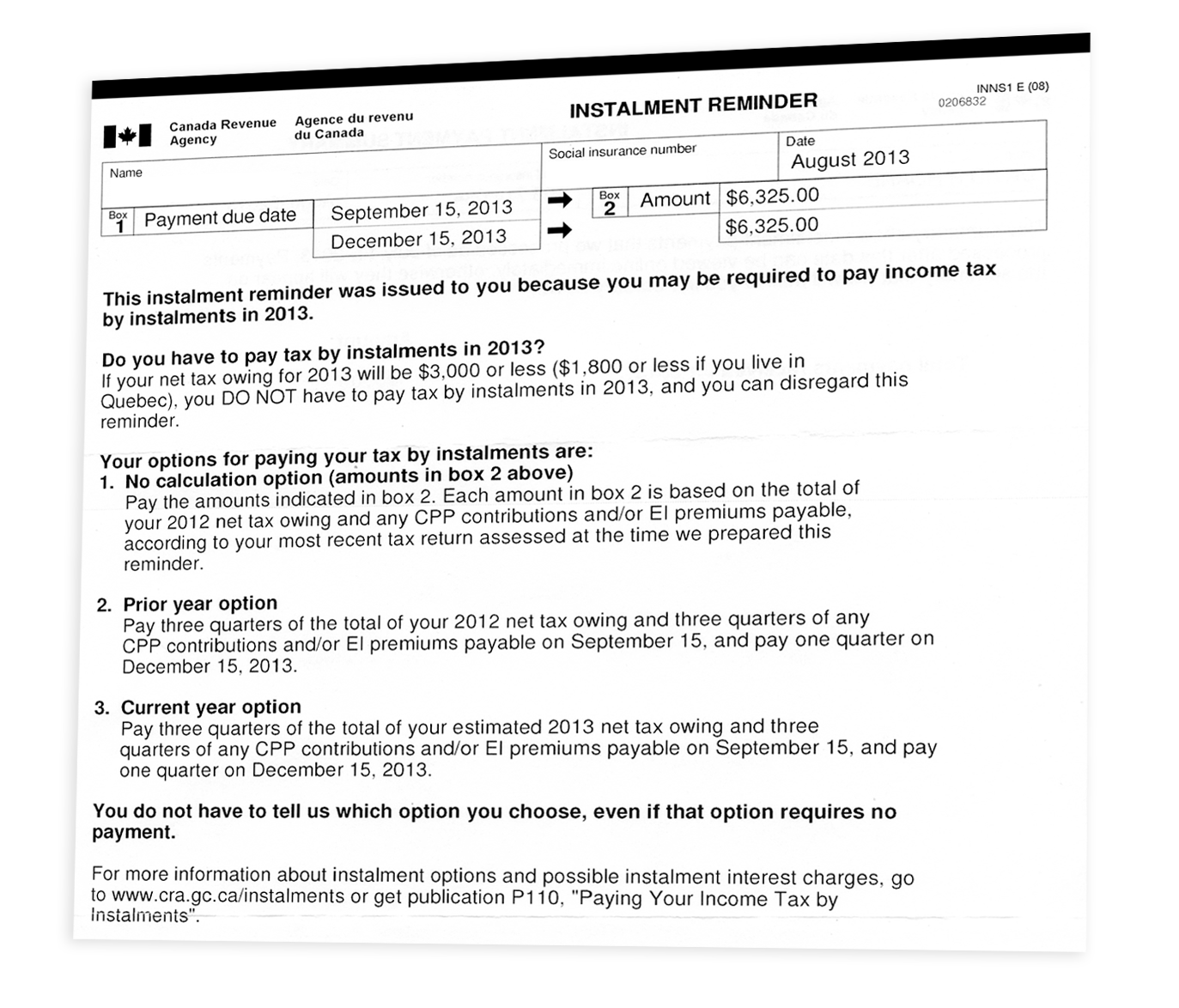

Figure 1: Sample Instalment Reminder Issued to Individuals by the Canada Revenue Agency

How do I calculate tax instalments if my income has increased or decreased compared to last year?

If your income remained the same this year as last year, or you expect your income to increase this year, you would be well advised to pay the amounts in the instalment reminder.

If your income is lower than it was in the prior year, CRA permits you to perform your own tax calculation and remit instalments based upon your own calculations. If your estimates err on the high end and you pay instalments in excess of what was required, then the CRA will issue a refund upon filing your tax return, and you will avoid deficient installment interest and/or penalties as a result.

However, if your income tax calculation is too low and instalment payments insufficient, then the result will be the imposition of deficient instalment interest and possibly deficient instalment penalties. You will want to avoid this.

What happens if the method of earning my income has changed?

For example, what happens if you’ve switched from earning dividend income to earning a salary?

Often, clients will ask, “I don’t need to bother paying this instalment now, since taxes are being withheld from my paycheque. I can ignore this, right?”

Not necessarily. There are a couple of instances in which installment payments may still be necessary.

- If you’ve received capital gains because you sold some stock or you have some interest income or dividend income, income tax will not be withheld at the time it’s earned. So, if the CRA has given notification that instalments are due and you haven’t responded with an instalment payment to cover the tax on your additional income, you’re setting yourself up for deficient instalment interest and possibly penalties.

- If you’ve withdrawn money over and above your salary from your corporation, this excess amount could result in additional income in the form of a dividend. This extra income will not have income tax withheld; therefore, you will not have paid sufficient income tax. As a result, you will incur deficient instalment interest and possibly penalties.

- If your income includes benefits such as CERB or Pregnancy and Parental Leave Benefits (“PPLPB”), you may find yourself in a situation where you’ve earned income on which income tax was not withheld at source. If that’s the case and you’ve received an instalment reminder, you are obliged to make an instalment payment. If you don’t respond with a payment, you could find yourself facing deficient instalment interest and possibly deficient instalment penalties.

So be careful. Consider whether or not you have additional sources of income that are not subject to tax at source and remit instalments accordingly.

Should I wait and see if I should pay instalments?

This is another common question. CRA instalment reminders are sent out twice a year: once in January/February and again in July/ August. So, some clients think, “Why don’t I wait and see if I’ve earned extra income to determine if I should make an instalment payment”. If you take this approach and an unexpected source of income occurs during the year, deficient installment interest and/or penalties will be assessed from the date that the original instalment amount was due.

Set up healthy habits around paying instalments

First, regularly log into your CRA “My Account” portal if that’s how you receive notifications. Or, keep an eye on your mail, if your CRA correspondence is received in this fashion. To ensure you don’t miss instalment payments, you can put a date in your calendar as a recurring reminder on March 1st, June 1st, September 1st, and December 1st to check to see if you have to make a payment.

Make sure the payments are received by CRA no later than the 15th of the month specified; otherwise, you’ll be late. We suggest you make payments by the 10th of the month to ensure they reach CRA in time.